Hi,

Welcome to my first english article. I have prepared drafts/deep dives about new companies that I will publish soon, but can’t release them yet as this blog became bigger and they are super illiquid and accumulation of shares continue. We will get to them in the future. Instead of that, I will go today back to the company I wrote about and owned. The thesis worked exactly as I assumed and lined up. I don’t know how many times that happens, so I would like to go back to my decision making process because I actually have not profit from this opportunity, but made much more money selling the company. First, if you have not seen it yet, here is my write-up from september 2023. Unfortunately it is written in Czech, so you will need to translate it (not a problem in today’s world). This article is for revisiting my decision making process, one thing very admired by Michael Mauboussin. I believe every investor should to that. It should also serve as a case study. Sometimes the best thing is to go backwards and see what really happened. Back to the analysis.

I said something like this:

“Today's analysis is about a company that is very cheap at first glance and extremely cheap for a Private Equity buyer, which many investors don't consider. However, no one knows when the company will eventually be sold. As is well known, investing is an art, not a science.”

Yet, this happened this May. The company got acquired with a huge premium of 73.8% from previous day's closing price and 87% up from my write-up and initial position at $7.7. Nice win you may say however I have not enjoyed this one and that is totally okay.

Why I got interested?

The main reason I got the initial interest in the company was announecement of “Expolartion of strategic alternatives” which I was on the hunt for (Looking for changes). At that time I did not really know that in 95% of these cases end up in tears. (Hey, Gee Group). One needs to be really sure that shareholders are at the top of management’s interest. I was sure about it here. On the board was a well known jockey I follow closely, Tim Eriksen. He has a long history of market outperformance and he always treat shareholders how they should be treated.

After doing further work I got to know few important things that made me feel selling the company is the most likely outcome. At that time after covid, staffing was on fire. Companies had shortage of labor and needed them to fulfill important places. 2022 was the year of highest number of acquisitions in the history and IT, the segment company operated in, the most active. Then I got to know that there were two external activist with combined ownership of 46% were involved in the company and for number of years being locked due to the illiquidity and trying to take over the company in 2017, when the company was lead by old management destroying value. TSRI was 59% position for the biggest owner. They really wanted to unlock the value. The second thing that was clear was the compensation package of CFO he would get if the company gets sold. The third was halting the buybacks.

With all these I was almost sure I knew what was going to happen but couldn’t tell when it will happen. “What” is far easier to predict than “when”. It was a game of probabilities, like the investing as a whole is.

Downside was low

The next thing was to think about valuation and what price was possible to get. The first thing was to look down and see what can I lose. This wasn’t a bipolar case stock. The exact price mattered. Buying it at 20% more would greatly impact the returns as it was not really a growing company. The only thing I counted on was a small increase of earning power and majority of my returns coming from multiple expansion. At the time of writing my analysis, the company was super cheap on net assets. It had NCAV of about $6 a share. I was buying at $7.7. The downside was low and I expected to actually grow the NCAV as most of non-recurring expensises, like litigation, was eliminated. On top of that the company was shifting to higher margin IT segment so I predicted small growth of earnings. It happened. Before being sold, the NCAV rose to $6.9 as I predicted.

I wrote: “So what's the downside? NCAV is roughly $6 per share and consists mainly of cash and quality receivables. Since the company has no long-term liabilities and it's getting operationally better I don't think it should be trading anywhere near its liquidation value. In addition, I estimate that this NCAV will continue to grow. The downside from this price is minimal, which is why I like this situation.”

What value could the company be sold at?

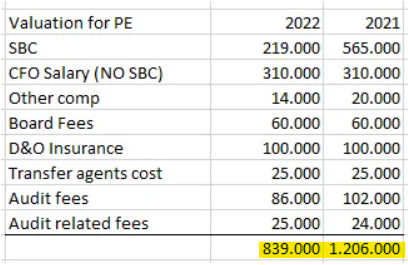

After getting the downside right, the next thing was to look at the upside. Apart from the great asset base, I thought making $2m of FCF per year was achieavable target as company in the previous year did. And if you look above, it clearly was right thing to assume. The valuation was 4.6x EV/FCF, quite compelling if you don’t discount the cash. I also tried to understand what expenses would be saved for private buyer as the company was very small & subscale. I figured out that adjusted for these expenses, the valuation is close to EV/FCF 2.9x.

I wrote: “In my opinion, management is putting itself in a position where it wants to sell TSRI. Long-term shareholder Zeff Capital is trying to do the same, but they can’t simply leave the position due to illiquidity and the fact that it would have to significantly reduce the share price. Acquisitions do not take place at exorbitant multiples. On the average, according to my knowledge, it is about 6-7x EV/EBITDA, however, it is not fixed and depends on several factors. Current EBITDA was $3m, cash 8m, implying a company value of $26-29m and a price per share of $11.6-13.” So I predicted mid-way price of $12.3, but that was when the cash balance was $8m, it was a price then. I said that at the end of its fiscal year, they will likely have $9.5-10m of cash on the balance sheet. No more non-recurring expenses. The company had exact $9.7m of net cash. Now it is even more after collecting receivables in downturn. Also the company repurchased some stock, so the upside changed by that $1.7m to $27.7-30.7m. The company was acquired for $29m. All worked as lined up.

What did I do and Why?

I sold at a $9 a share, or something like 17% profit. I have not enjoyed the full upside even though I was sure that I got valuation somewhat right. There were two things that forced me to sell. First was the opportunity cost. I figured out that this was not one of the better ideas I had, it did not have multibagger potential. I moved the proceeds to Alarum which has performed beautifully and currently sits at 8 bagger. It was total opposite to TSRI. It had much better economics, extreme growth and scale down of loss-making business should show the great improvement of earnings power, while trading at single digit multiple. TSRI had nothing like that apart trading at similar multiple, not considering the cash. It had only downside protection but much lower expected values. The decision was clear by this. But there was a second impact. Staffing as a whole industry is cyclical and got into the downturn as economy cooled down and low unemployment rates made it hard for staffing companies who typically experience churn of labor of 20-30% annualy. It wasn’t just TSRI, but in general the whole staffing industry experiences rough time. I watched other staffing companies and I did not know how long it will last. Revenues started to decline, so I was worried this would impact the attractivity of acquiring TSRI and getting to the full expected value as the company even reported some losses the next quarter and given the 4 customer accounted for 65% of sales + losing a customer in the past, I decided to move on. The “When” got into my thesis and I did not want to wait few years given what opportunities are currently out there in Micro-Cap space. So in the end I think, my general decision making process regarding the investment was right. It was just tough to see suddenly when the sale will happen and I was assuming it may take longer than initially expected as facts changed. I was betting on the jockey, fold down, and the jockey proved me wrong and deserved all the glory by those, who did not leave their seats and saw him winning the race, while I already left playing elsewhere. I am glad it happened.

The presentation is not an investment recommendation. It is for educational purposes only.

Thank you for your criticism, feedback or discussion,

Jacob

This post is free for everyone, but if you value my work and would like to support me, you can do it here:

You might like to look at IRIX in a similar situation