Why I passed on Quorum Information Technologies

Hi,

I was thinking a lot about sharing my work on companies, that I found interesting but decided not to invest in them (for now). You can call them watchlist ideas, but I stick mainly to reasoning that idea (or speculation) is a good one or it is not. Of course many speculations can grow into investments and I am not saying that these wont be investible in future. But profiling them will help me to structure my thinking and see potential changes, or perhaps the main goal is to get smarter in investing by also telling why I have not invested in a particular company. I will try to keep these shorther than regular deep dives, which I would like to complement with this format. I always want to hear the bear case of any person in companies that I own. So this is something I would also ask from you for my investments.

The company I passed on is Qourum Information Technologies, ticker is $QIS.V. It is a canadian company not very well known. Quick overview of the valuation and main matrics looks like this (all in CAD):

Share Price: $0.94

Shares Outstanding: 73.5m

Market Cap (MM): $69.14m

Net Debt (MM): $3.7m

Enterprise Value (MM): $72.84m

LTM EBITDA (MM): $7.6m

EV/EBITDA: 9.6x

EV/ARR: 2.4x

Foundation date: 1996

This is classic company that scored very highly after going 2x through all canadian companies in my list. It is software company (altough not that high gross margin), that has interesting board member with ties to CSU (Damien Leonard, the son of Mark Leonard), announced cost cutting and change in the strategy. All that sounds really interesting for 9.6x EBITDA and founder led company. And on top of that, customers are super sticky. + I learned a lot about dealerships operations this year, so I might consider it in my circle of competence. However. There are reasons to think this is not a good investment idea and I would like to adress those.

About

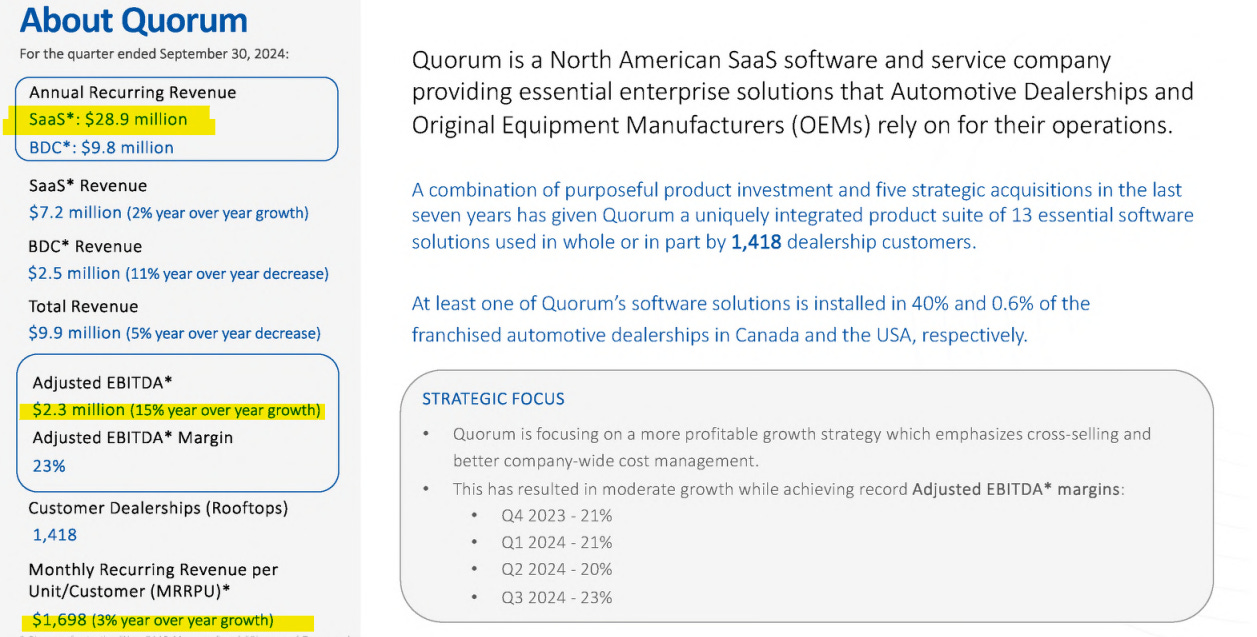

Quorum Information Technologies is a software provider of DMS (Dealership management system) for automotive dealerships in Canada and United States. The company has 35 software developers. The company owns a number of products that they got to own by acquiring. The company develops, markets, implements, and supports software products for the automotive market, including Quorum DMS, a classic dealership management system. Its core product is Autovance Desk, which is a modern retailing platform that aids dealerships in attracting business through digital channels. It features tools for desking, menu solutions for finance and insurance. The second core product is DealerMine which is a CRM system that supports both sales and service departments within dealerships. The third main one is VINN Automotive, which is a marketplace designed to simplify the vehicle research and purchasing process for consumers while enabling retailers to sell more efficiently. In total, they have about 13 products. Qourum is part of the DMS software that runs daily operations mainly in Canadian dealerships. DMS is an enterprise resource planning (ERP) product for dealerships, which tends to be super sticky. Quorum also provides Business Development Centre (“BDC” - part of their CRM) or call centre services to help dealerships drive business into their service departments. One such customer is the AutoCanada BDC that is operated by Quorum under a long-standing strategic partnership between the companies. Dealerships that are Service CRM software customers also have the option of outsourcing their BDC needs to Quorum. For them, the BDC is mainly for service side of the dealership (sales side x service side). BDC makes calls to book customers for service points. They never sell their BDC service without selling their software as well. Every BDC customer has their CRM service software even if it should be absolute minimum. They were focused on improving BDC margins by outsourcing staffing (away from Canada, pushed remaining employees to do a better job, but still considering to outsource part of software development team, because it is cheaper and they even have done better job) , which worked really well and was main driver of overal cost cutting program. On a question if there are costs that could be further cut on a C-level, the answer was just simply “no”.

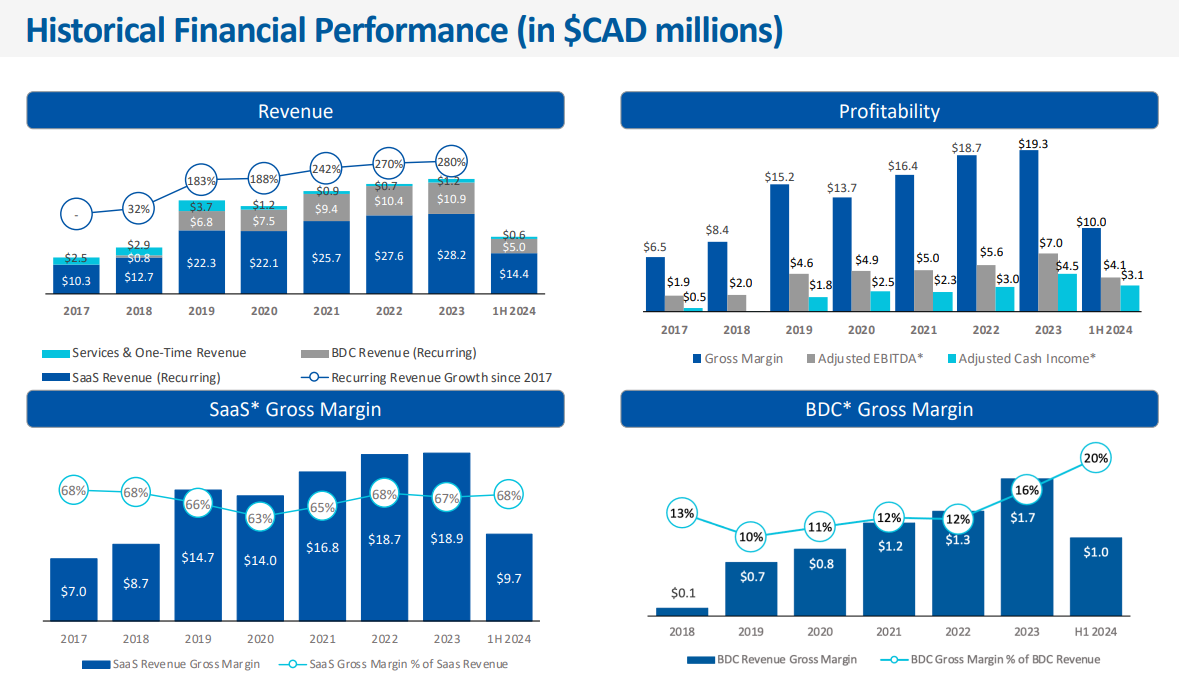

The next thing for BDC is AI, which can help with outreach and initial contact with customers. They want AI to replace agents who do the calls. They already started the investment and already had “some wins”. In ideal world, they could double the gross margins within BDC business from here. And the CEO wants it to be maningful part of the business, because it also increases the stickinnes for their software. “Right now, it is a big of a drag on our business and I need to fix that.” They got into their current position by acquiring a number of companies, which helped them expanding rooftops from 420 in 2017 to current 1400. Quorum’s revenues are primarily SaaS-based monthly recurring revenues. They report two business lines. SaaS and BDC. SaaS has 67% GM while BDC has 20%. SaaS is 73% of revenues and growing slowly (recently 2% YoY growth) and BDC is declining (recently 11% decline). Given the cost optimization (all expenses are going down, R&D, S&M,..) they have been able to grow EBITDA margins to 20% from 10% on a C-level. Their products have very different price ranges. Their DMS would sell for anywhere near $1500-3500/month. AutoVance about $500/month, … They dont specify which is their best product (I suspect AutoVance, and not the DMS), because they dont want to disclose that to competitors. CEO said that not all of their products could be sold to all the dealerships. There are OEMs which they can not sell the product to, because they need to be certified by the OEM. There is not any product they would like to sell that they would need to develop themselves.

A bit of the history

Started as ERP business which is difficult - lots of moving pieces - managing inventory, managing service side, sell side, technicians, all the accounting, CRM, they have to integrate into the factories (GM, Toyotas,..). If they would know how hard work it was, they would pick different vertical = barrier to entry for newcomers? - Every dealership has also their own reporting systems and communicates differently.

They quickly learned that every dealership they went to, had multiple other 3rd party solutions, so they would always need to build integration to all these 3rd party solutions so they started to build “3rd party solutions” themselves. So after years of doing installs they started. Built numerous products. But they couldnt do just building and building. They realized the dealership has 25 different vendors to run their business and that morphed them into an acquisition driven strategy. First acquisition in 2017….

Acquisitions

in August 2017 with its acquisition of Autovance Technologies Inc., which provides vehicle sales Digital Retailing, Desking and F&I Menu solutions to help dealerships seamlessly present payment, lease and financing information to customers in person and online. What CEO said is that they have a big opportunity to cross-sell even within their brands like Autovance is. AutoVance comprises of 3 products and not all customers have all 3. Then they have the opportunity to cross-sell it to DMS customers (40% of dealerships currently use the AutoVance I believe) There is multiple ways to cross-sell. AutoVance does not require some size specifics of dealerships.

In October 2018, Quorum completed the transformative acquisition of DealerMine Inc. The DealerMine acquisition significantly accelerated Quorum’s strategic vision to be a full-service provider to automotive dealerships by adding DealerMine’s Service CRM (Customer Relationship Management). They acquired DealerMine which had over 500 customers.

On April 1, 2022, Quorum acquired Accessible Accessories Ltd., headquartered in Medicine Hat, Alberta, Canada. Accessible develops, implements, and supports its web-based platform that allows franchised dealerships to sell accessories more effectively. Had over 680 automotive franchised dealership customers across Canada.

June 23 2023, completing the acquisition with VINN Automotive Technologies Limited. This has expanded Quorum's reach into the Business to Consumer (B2C) market as VINN is a premier automotive marketplace that streamlines the vehicle research and purchase process for vehicle shoppers while helping retailers sell more efficiently.

“So opportunity #1 for us was just being more complete in how we - more complete and consistent in how we did price increases across our customer base and across all of our different brands. After acquiring different companies, we had different price increase policies and so we consolidated those. And just we're a lot more diligent about putting consistent price increases across our entire customer base across all our brands. So that was number one. Number two, on our DMS product, we've also been more consistent on moving our DMS customers to our per user MSRP pricing. So we've done that as part of the transition work that we've been doing throughout the season -- throughout this year. And yes, those are the 2 primary things.”"

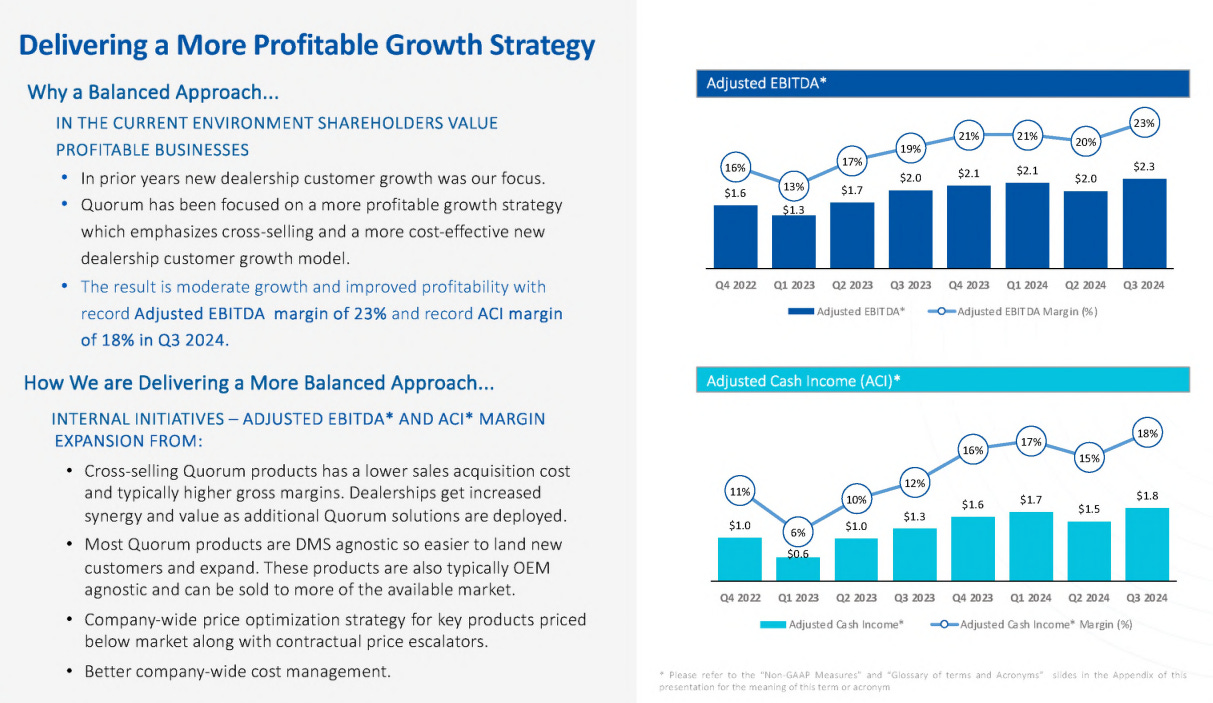

In 2022, Quorum completed the process of integrating its strategic acquisitions (all these were canadian acquisitions and all had their customer base), which included moving from a divisional business model to a functional business model with a single "One Quorum” team. These acquisitions helped to increase the range (dealerships rooftops). However they needed to change strategy because going for the rooftops was costly and decided to go for cross-selling, which saves a lot of on the cost side. The rapid integration of new businesses has led to organizational redundancies and inefficient resource allocation, resulting in cash margins remaining below 10% over the past few years. Their cost cutting worked well and cash flow increased nicely. They were not money-losing company anymore. EBITDA margins, which was and still is their main focus, increased from 10% to 20%, typical scaling software company. They used this generated cash flows to almost pay down their expensive debt of 9.5-12.5%. Going forward they are primarily focused on cross-selling because it should be less costly way to gain new business, or at least in theory. Quorum’s product suite currently covers 13 of the 25 most common categories for dealership operations. They have at least 1 product in 40% dealerships across Canada, which brings in majority of sales and they sell on average 1.5 product per dealership. But in total they have 13 products which they can cross-sell. And here is the problem.

The underperformance prior 2023 attracted the attention of activist investors, notably Damien Leonard of Pinetree Capital, who secured a board seat in June 2023. Pinetree Capital owns 25% of the company. Voss Capital owns 20%. Founder owns 3.2%. Damien has been investor in Quorum for number of years. They were changing ideas regarding capital allocation and strategy with them.

Cross-selling Opportunity

Their X-selling opp backs out the OEMs they can not sell to. It is mainly within what they already have. Another thing is that their DealerMine product does not work well within small franchised stores. It works better within mid-sized and larger stores (needs more traffic to be useful) and they back this out of ther X-Selling target.

The problem

One of the biggest hurdles Quorum faces is that switching costs are extremely high in this industry, becuase there are lots of decision makers around the product use (for DMS it is sales manager, services manager, parts manager, controller, dealer, principal and others - super long sales process, for non-DMS products, it is sales manager and business manager which shortens the sales process, but I suspect that dealerships build typically around their DMS and Quourum targets smaller dealerships with their DMS, so this could be scale problem too). You would say, well that is good competitive advantage to have. But it also means it is super tough to gain market share or replace products from other providers if there are large switching costs! On top of that the dealership would take significant operational risk and it would need to train all of their employees to a new software. Back to what they say. They think if they would get to a level of their top selling product, they would gain $54m of aditional revenue, and to be honest, that would make this wonderful investment. Their products on average are 40% cheaper than of the competitors for DMS functionality (even though it is modules/volume based, but dealership can negotiate a lot on the price). Do they want to close the pricing gap? Have not looked into it. They are still experimenting with pricing bundles. However even with massive recent tailwinds, they have been unable to cross-sell at any meaningful pace. I would structure it into few pieces. Quick screen on Reddit suggests that many people do not know about Qourum and people in the industry prefer to use their competitors.

The industry is dominated by two top players

A key problem for vehicle dealerships is that they typically use many disparate solutions across 25 different categories of software solutions and over 700 vendor’s software within those categories to run their business. Both Reynolds and CDK are almost in all 25 categories and have about 85% market share.

His opinion on Rey&Rey and CDK is that CDK was always a tougher competitor. They are willing to negotiate more. Rey&Rey is somewhat difficult company to do business with, there are multiple lawsuits against them by dealerships because of some screw-offs. They should have number of years left in them, but innovation is super poor. Another competitor is Tekion which is very innovative and has loads of cash. Mauri is worried about every competitor with lots of cash and I do not like them being an ant when competitors can easily outspend them on R&D. Tekion is becoming a threat to them (his words) and it is growing quickly and gaining rooftops through also not asking for integration costs, while others do. The amount of capital top players have can not be compared to Quourum, which is very capital constrained and that impacts innovation in all aspects.

One of them was facing a significant challenge

CDK was a target of the cyber attack this summer, which led to losses of approximately $605m for dealerships in 2 weeks during the attack. Even though Aaryn (CEO of Connexion Mobility) told me that they have seen some customers churning, it was pretty insignificant and Qourum has not seen any major increase from this opportunity to gain churning customers off leading company (MRRPU barely increased, which is basically all they focus on currently). And you would think otherwise would happen, given that this impacted almost the whole industry and caused massive losses. It was clearly opportunity for other companies, but Qourum seems like they do not have what it needs.

When talking with the CEO he said he wished he would not get into the software business. And it makes sense. When asked about if they would gain business against competitors like Rey and CDK when switching costs are so high, Mauri answered that they obviously would like to go to the dealerships and show them their products and sell to them but it is a tough sale, when you need to get everybody on board, all the managers of dealership on board and they would need to go through a big change. They would wish to go and let customers try 1-2 products, then 3-4 and then they would ask them to try out their DMS, a product dealerships spend the most on. On a question if it actually can happen, he answered that is something they learned to be very patient about (translate it as you wish, but I wonder..). Then he said that getting a product utilized in a dealership is a challenge. “No matter how well it is designed and how good is support around it, it is a challenge to get the staff to adopt products.” This confirms the thesis around the switching costs further.

What they want to do going forward

After paying down the debt, they would like to pursue the acquistion story again, which would be complement to selling add-ons and cross-selling. What they found out previously when they built their own products was that it was very hard to sell it at retail price. This was much easier when they acquired the product which already had its customers. But to the future. Mauri talks about the US market is so massive and they would like to enter it, because it is also higher gross margin business. Rooftops is 19600 for US against 3200 in Canada = much bigger TAM. But it is also more expensive to go after and it has lots of risks. And they are interested a lot in doing some acquisition in the US. A market where they have only a bit of revenues and small number of rooftops. The market which they do not have a deep knowledge about compared to Canada and it is much more competitive. Mauri talks about a need to change their acquisition strategy to go there. And with that, there are lots of unknowns. And I do not like to take this risk alongside with super low organic growth. It also requires completely new marketing strategy. US marketplace is much more complex. More banks you can do deals with, more different companies that you may buy, warranty, insurance for vehicles. Much more efficient market with lots of liquidity. In Canada they need to build the integration with the OEM before they can sell. For the US it would require very big investment. Why not just focuse on cross-selling first, which is lagging a lot? Talking about strategic fits dont help my confidence. They have not taken the decision yet, whether to do buybacks or pay dividends when they retire the debt. This thesis is heavily dependent on management’s execution. The Quroum is also not known in the US. Potential customers do not know them. There were some cases that providers went to the US and they did not get the results they wanted. Quorum could burn money here, but that shall be seen how they decide.

Some Financial things

Top line is known. Mainly grew from acquisitions. Cost cuts they did is also known. They do not think they can not cut it anymore - maybe after doing more workforce outsourcing.

Their amortization for internally developed intangibles is 10 years, which immediately striked me. I think I have not seen this long amortization for software companies. I would bet that is really overstated. Even though the level of innovation is probably not that high. The company had really expensive debt carrying 9.5% and 12.5% which they almost fully paid down.

Their services segment is running at negative numbers, but that is mostly customization and implementation revenue and should not be recurring in theory. But they will continue doing these. The amount of effort and cost dealerships take especially in their DMS product type would prevent a sale. And their competitors discount upfronts heavily. For Quorum to remain competitive, they need to discount those costs. They are cautious of how much they do, but it is and it will remain negative gross margin business, which could impact any year’s financials. The only way to improve the margins here is to sell more training, but it is not high priority force at this stage.

What I would like to see to change my mind

Seeing BDC margins to expand even more with successful AI implementation. This could trigger some things as canadian dealership industry is quite underinvested compared to the US. Investors also typically get excited about rising margins. But is there a need to push the innovation a lot in much smaller industry?

Growth will pick up as a successful cross-selling sign combined with milking the business by top competitors. Current price of 2.4x EV/ARR does not expect the growth picking up. + There are lots of ways to potential growth. —> New OEMs certifications, selling new products to existing customers, selling new products to new customers, acquiring new products with existing customer base,… but at this point, I highly doubt we will see high organic growth.

I would welcome some kind of cash returns. I think probability of this is high when the debt will be fully paid off. I am just not sure on % being paid out.

Review

Even though me being sceptical, I think there is a serious potential for this investment to work out. They trade at very reasonable multiple of around 9.6x EV/EBITDA what sounds like sticky business and I would expect that they might become acquisition target at this price. However they also capitalize intangibles, so free cash flow is lower than reported ebitda and also they are using it to pay down the debt for now. But soon this burden should be released and the company will decide what to do with cash. I do not like that they are the ant in the industry and that the growth is just too low, opposite of what I like to see in SaaS. I am using $5.5m of current earnings power after capitalized intangibles (which depends on their spending rate), which would suggest 7.5% return per year and I think they can grow overal 3% if growth wont pick up. I think investors would earn reasonable 10% return, which is not enough for me, so I need to pass on it here. However, I will monitorate closely. Because if only one change occurs, it could get very interesting.

The presentation is not an investment recommendation. It is for educational purposes only.

Thank you for your criticism, feedback or discussion,

Jacob

This post is free for everyone, but if you value my work and would like to buy me a coffee, you can do it here:

At some point (2012-2015) they generated 1/3 of their revenue with GM in the US using only their XSellerate DMS. They have more experience with integration there then they are given credit. One of the peculiarities of non-DMS products is that they pay integration costs to other DMS providers. For example PBS DMS is integrated with Dealermine CRM (they list it as partnership). Check this source for example: https://www.pbssystems.com/partners

Now there are so many of these small affiliate software companies that for Quorum, it would be the smartest to target non DMS offerings that are integrated with most common DMS providers among their existing rooftops. I managed to find close to 400 here alone https://www.capterra.com/auto-dealer-software/?features=3990e00b-853e-41a0-a871-33607f212727&sort=alphabetical.

If they manage this, it would count as a cross sell (but through acquisition). If they do it smart, it could earn them a high marginal ROIC. I would assume Damien would veto bad ideas, Alternatively, they could cut on integration cash outflow (capitalized R&D) and start paying 10% dividend. Or just cumulate cash and be acquired by likes of CDK, PBS or Dealertrack.

I am still digging around to see what are they doing with investment tax credits and loans from ACOA, but they seem fairly valued for a stable business which they can be at even lower cost. As you mention, there are barriers to entry, but they also protect them if they want to be a cash cow.

Appreciate the detailed breakdown! The cost cutting efforts and AI push sound promising but with BDC revenue declining and SaaS growth barely moving, do you think their cross-selling strategy is enough to reignite growth?