RJD Holdings - Ugly but cheap

Hi,

And welcome to my new article. This will be a shorter one and definitely not a deep dive like with higher quality companies. This is just a bet on a cheap stock, which I tend to do with lower expoure in my portfolio and traded this in the past quite successfully. It is not fully a business analysis, but rather cigar butt opportunity. There is nothing special about this company, only valuation so please be careful as earnings can change quite quickly with these type of companies with no moat or whatsoever. Risk management aka position sizing is the key. If you hold 5-10 of these, I think it can produce good results combined. Definitely not bet your life savings here and do not rely on this write-up as I consider it being an ugly company, potentially good trade. I differentiate between trades and investments and this one is just a trade for me. However I tend to have super high hurdle when investing in micro-caps. Either buy growing company for no-growth multiple or I buy super cheap stuff at less than 5x earnings. This one is even less than that. I would not buy these at 7x earnings. If you don’t find this interesting, there is no need to worry. My pipeline is full of ideas and I have prepared drafts with deep dives on the “investments” type. The company I will profile is not a one to hold forever. I sold in the past for 70% profit in several months and rebought again as I didn’t think latest results are being appreciated enough. First buy was at $0.0062, and with an average of $0.0074 I sold at $0.0125. In the recent times I rebought at $0.0097 and then again sold at $0.013 some. Current share price is $0.0108 and I hold small position still. This is not originally my idea, but one extraordinary man who brought the company to me and allowed me to write it up. Be aware that information is pretty constraint on this one, but it is real business producing real cash flows. All press-releases go back to 2016 and that is what I did, and even with that I have more questions than answers. As I was a very sceptical during all of the reading, I ask myself: “Is this analysis?” Sometimes it looks like I don’t even like the company.

WARNING: This is sub $5m company, and shares are very illiquid. Make sure you are very prudent with your limit trades if you decide to buy based on your DD. Small volume buys can make this stock to rise a lot and I can obviously profit from that.

Share Price: $0.0108

Shares Oustanding: 359.36m

Market Cap: $3.88m

Net Cash: $2.044m

Enterprise Value: $1.83m

Q1-Q3 EBIT: $1.078m

EBIT Q3: $550k

NCAV: $2.781m

NCAV per share: $0.0072

Insider ownership: 23.45%

Business

The holding company was formed in 2009. Their business has 3 holdings in industries like construction, healthcare & environmental and each operating decentralized. Strange combination but whatever. The most important one and which I will focus on is Silex Holdings, a regional player in Oklahoma with two locations in Edmonton and Tulsa, which is involved in the construction products business which they manufacture, distribute and install in the high end houses. Silex Interiors, fills a market niche between the Home Depots and local homebuilders. Silex manufactures and installs granite/other counter tops, cabinets and related products to the residential builder, commercial contractor, remodel contractor and DIY customer. Silex Interiors was formed in 2006 to fabricate and install hard surface countertops for kitchens and baths. Originally located in Tulsa, Silex announced the first franchise sale of the Silex Interiors, an additional location in Edmond Oklahoma to provide products and services to the entire state of Oklahoma in 2016. Silex was purchased in 2012 by Southbridge Advisory Group, Inc. RJD Green acquired Silex in 2015 from Southbridge where the CEO was a managing director and where he probably learnt “getting bigger complex”, pursuing growth through acquisitions. The company issued shares for the sellers in respect to this acquisition. Today, Silex Interiors offers full services for kitchens, living rooms and baths to all market sectors. Originally it had one selling/distributing location but added second along they way. In 2015 they got partnership with US new homes manufacturer DR Horton for 18 months. In 2017 they were awarded a Preferred Vendor contract for eastern Oklahoma for countertop manufacturing and installation from the Affiliated Builders Group. They are getting orderds from regional homebuilders and are heavily dependent on commercical projects. They are volume bidder focusing on larger multi-family projects in the high-end custom home market. In the past they have been able to maintain or grow in a tougher environment for home builders given the high-end focus.

Yes, this pico-cap is a real business…

Here are some detailed photos for understanding the products.

They are launching new products and focusing on add-ons like fireplaces, solid surfaces (not stone), and couple more things which they have not announced yet. Silex Holdings capital investment totaled over $500,000 and includes CNC fully automated saws and templating equipment, online polishing equipment, additional fabrication facility improvements, along with wet shop upgrades. Their focus are high-end custom homes $1,000,000 to $30,000,000 which should prevent some cyclicality.

I am not sure whether I should spend time with other two divisions, which clearly are super irrelevant in terms of revenue & investments, but just a quick description, so one can fully develop his picture and feelings.

Immediately after current CEO got into the lead, he acquired the company called IOSOFT Inc., which marks the first healthcare services acquisition of RJD Green. IOSOFT was formed in 1998 by current principal, Vincent Valentine, to provide proprietary software for medical billing, Healthcare claims adjudication, automotive warranty payments, and electronic payments between healthcare Payers and Providers, and several other platform developments. Since formation, IOSOFT has been a third-party developer of software and provides IT support for the platforms developed. Most of the Company’s efforts have been healthcare oriented in paperless claim filing and provider payment services. IOSOFT’s existing three-year mean annual EBITDA was $182,297 at the time of acquisition but I did not find purchase price, nor I have not noticed any recent numbers, apart time to time mentioning some contracts.

At the time of 2016 the company was also involved in Animal Waste Management where they claimed that they have patented technology, which addresses environmental issues of the commercial hog and poultry farm by eliminating liquid, solid, and gas waste while returning the water to usable ground water on the farm at cost similar to the handling and transporting expense of current waste disposal. In 2018 they acquired the twelve-acre industrial property utilized for an initial animal waste processing facility. Again, I don’t think this generates revenues and won’t spend my time with that.

Management

I like the ownership of the management here, which did not change for the last few years. They own 23.45%. We will get to how they got to owning such a high stake.

For the comparison this is ownership from 2020

They are super lazy coming up with press releases with common mistakes in them like using the same number for operating profits and cash balance. It did not happen once, so one needs to look deeper to see what the financials are really like. On top of that, they were quite promotional in the past, setting targets which never could be met with tons of press releases. I think they learnt the way, and started to get investor awareness different way.

It was revenue…

There are literally ton of press releases like these

Also when one looks at their website, he immediately spots the focus on acquisitions they want to make. I think it is definitively risk, because the cash could be better deployed. But given the cheap valuation I am able to accept that. If the earnings would not be that strong, it would not be that compelling. CEO is Ron Brewer who owns 11% of this business. Management changed in 2016. Ron replaced Rex Washburn in 2016 when he resigned due to health issues, the same change occured for CFO. Ron has served as a corporate officer in both public and private companies and has obviously m&a background since he was at Southbridge which sold Silex to RJD. The CFO is John Rabbitt who was also involved in acquisitions. He was involved in a company that has grown revenues from $20m to $850m in 9 years until it got acquired by PepsiCo. He also served as a member of PepsiCo’s Mid-West Advisory Board, and as a Director and Secretary/Treasurer of their largest canning division.

Share issuance in the past

In 2016 & 2017 there was share issuance in respect to retire the debt which was callable on demand. The company was retiring debt with share issuance and also at the time the company had liquidity issues and even got donations from its directors to survive. Then the Company issued 63,127,338 restricted shares to RJD Green Inc. officers Ron Brewer, Jerry Niblett, and John Rabbitt retiring $688,088 of accrued salaries. Stock was issued at market price in May 17, 2021. The company has not diluted since retiring the accrued salaries. What was the reason? They had not been taking any salaries since acquiring the company. These shares for management were issued at $0.013 which is above current share price, totally recapitalizing its balance sheet. Since then, there are only a little of accrued salaries on the liability side.

Changing path of communication with investors..

The company set its IR this May to make them closer to investors who still are not probably aware of the company. On top of that CEO occured on the podcast for the first time in the history and the company made a tweet for the first time in two years. It is not super detailed, but it provides good insights about the near term future like uplisting, which should further help with increasing investor’s awareness. - Is this security analysis you probably wonder. Well it is not, but I think investors need to see the value here otherwise the shares could again be flat the next 2 years. They want to uplist to OTC.QB as early as next year which requires audited reporting and minimal $0.01 share price.

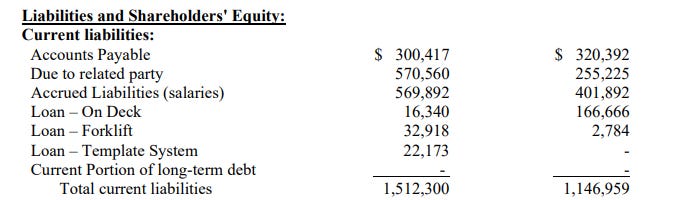

Financials

The company uses ARR, which I have really trouble with. There is probably anything but certain that this company has recurring revenues. They are getting contracts, so they are volume taker. They report their backlog, but they don’t do that every quarter so it is quite tough to get a sense around that. I tried to read every press release the company has given out and I get that the results are impacted a lot by large orders. This May for example was a record braking for the company. They did revenue of $865,730 with Net Operating profit of $242,404 which is like 3 average months of the past years. In 2017 they got one time orders in Kansas and Missouri. So there are obivously risks that these contracts will run out and the company won’t be able to replace them. But so far they have been doing a good job apart press releases.

This breakdown is only in latest annual report, so apologize not having everything at 1 sheet. There is not much to say about it. The company implemeted some inventory features 1 year back which resulted in savings of over $200k. The company is generating good profits especially recently. And given that accrued salaries were paid by shares, the company started to generate good cash flows. But main trigger was the last few quarters, which were especially good.

Most of their assets are current. Cash is building up quickly on the balance sheet and the company has $2m of cash without any long-term debt. Biggest liability is to vendors. During the last 9 months the company provided $1.3m from operating activities. To remember current Market Cap is $3.88m with $2.04m net cash. This is EV/FCF close to 1x. Again all depends on sustainability, but I think at this price, the worst case scenario might be priced in, if there is any given the illiquidity. Right now I think company might be slightly overarning as backlog was boosted by some big orders last year and the gross margins visually expanded a lot (could be due to scale and high-end custom housing focus), but I still think $800-1000k of earnings power is likely possible.

There are obviously good reasons why the company is cheap such as acquisition focus, press issues, potential cyclicality & past share issuance + current high number of shares oustanding. However one needs to admire that they have done a good job with what they have. I am not expecting this to trade at high multiple and I would sell if the P/E would expand closer to 6x. Also since current management is there, they have been profitable since and grew revenues from $2.9m to $5.7m LTM which is not bad. All while maintaining profitability and not diluting since 2021. And they target acquisitions at least in the same sector as their best division Silex.

Risks

The biggest risk I consider to happen is that management lights the cash up on some kind of stupid acquisition. I believe their networth is most of the equity holding in this company so not sure what the probability is. But the cash is their greatest asset that they hold and it is a important part of the “security” here. Doing something stupid with it would be a thesis braker as I am not 100% sure about that I can predict the earnings smoothly. CEO has decades of m&a background so one must not act surprised if he sees press release coming out.

The same level risk is that current earnings are overstated given the large contracts they received in the recent months. As I said, it is very tough to follow the backlog transforming to revenues as they report it like they want, but I think most of it gets billed in less than a year. Earnings are what makes this stock interesting. It is a cheap bet and if the earnings would deteorirate it would not put the company into liquidity troubles, but it would definitely impact attractivity of current undervaluation and I am not interested owning this anywhere close to fair value or just for the cash reason, which probably should is discounted by the market rightfully.

Overview

You probably have mixed feelings about the company and I understand that. It is just super small OTC listed stock with limited amount of information, wrong typos in press releases, two divisions which probably don’t generate any meaningful revenue. There are many things of what not to like but… the stock is cheap, probably too cheap (convincing myself to own a stock like this, haha). It is tough to make rational investment decision here apart from looking at numbers. I totally get that only fools look at numbers in isolation, but I am not betting much. This is not my ideal investment, but buying ugly stuff at 2-3x P/E generally works (worked for them, will work for us?). I was sceptical, whether I should write about this one, but given that I can not about other stuff yet, I took a risk and I am well aware that if this ends up badly, I will eat my lunch. But I also believe that people would suddenly like this stock after they see it doubling. You don’t find often high quality stuff at a price like this and I generally think quantity is quality in itself, but risk management here is definitely a key.

The presentation is not an investment recommendation. It is for educational purposes only.

Thank you for your criticism, feedback or discussion,

Jacob

This post is free for everyone, but if you value my work and would like to support me, you can do it here:

Interesting situation, thanks for the write-up! Indeed a bit ugly but it does look cheap. A year later earnings are still holding steady. There's been some activity with the launch of the JSI division and, more recently, the seed funding in Aspyr Living. Do you still follow the company?

Dear Jakub,

Thank you for another inspiring article. Although I primarily invest in ETFs, your articles provide valuable insights into different types of investing and teach me how to think critically about companies themselves. I have a one question for you, Iwas also wondering if you could briefly describe your approach to investing in such small companies. My broker doesn't offer these microcaps in their portfolio. Do you use a specific tool or platform for accessing them?

Best regards,

Tomas