F(u)natism

Investment Idea

Hello,

Over the last few weeks/months I have been looking into Japanese (mega)trends/themes to find the right investment. I think there are three trends (excluding the AI) hapenning at the same time that I have been able to identify.

1) Japan is aging and there are lots of companies benefitting from this trend. The best one to go with seems to be Kamakura Shinsho, which is the largest funeral/cemetery matching site in Japan. While the industry is mostly local and online share of handling end of life needs is negligible, as younger generations will age, Kamakura should sees the benefit as a partner of choice.

2) Mid-career change of jobs, since inflation came back to Japan, many people are assesing their alternatives and are not that loyal anymore to the initial employer. Japan is extremely short on workforce and companies spend more and more on looking for talent, which results in rising success fees. Given the shortage, employees are becoming scarce and scarcity is value. The bargaining power over their employers hence increased. This problem resulted in the rise of niche recruitment platforms and some of them acquired a real data advantage of having a database of reviews of the employees and companies. Mid-career is more volatile than new graduates, however I own one company that I believe is competetively advantaged in this theme but still waiting for the opportunity to publish my prepared write-up on this one.

3) Entertainment. I am seeing a boom of Japanese entertainment industry after covid collapse, which is a very rich in nature and offering unique experiences. Furthermore the entertainment industry in Japan essentially works as a religion, where people are truly loyal to their favourite artist or idol. There are number of companies I am highly interested in and in this write-up I will go one by one to sort it out.

After diving into largest funeral platform, the entertainment is a theme I am diving into today.

Vtubers

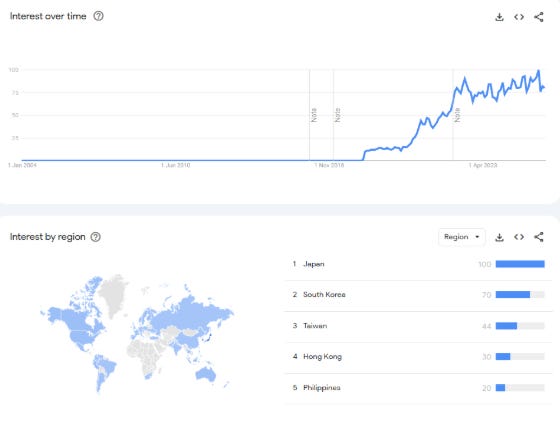

I have spent quite a lot of time on the theme that could be similar to Nicotine Pouches. Japan has developed essentially “idol ecosystem”, which is the most recently seen through Vtubers. I consider VTubing as a megatrend as since its start in Japan in mid 2010s and it spreaded like a virus across the country and now is spreading globally as a pheonemon. In case you do not know who the Vtuber is, it is a real person who performs streaming through its assigned anime character, which is usually owned by the Vtuber agency. I am sharing quick youtube video so you can see what I am talking about. You might think this is a fad or pandemic miracle— something that comes and goes— but it truly is not. Today there are over 10.000 Vtubers out there and they are making living off it.

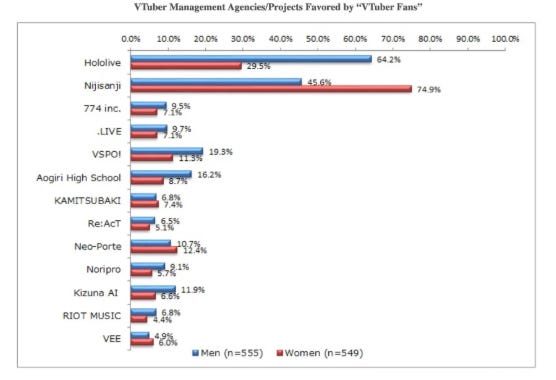

And given the people are usually weird, they absolutely love it, especially younger generations but also more increasingly adults. By 2025, VTubers had achieved global cultural penetration, with YouTube reporting 50 billion annual views and 57% of 14–44-year-olds watching virtual creators. They highlight that they can actually get closer to the Vtubers, something close to “Digital intimacy”. There are two companies to play this trend — Cover Corp and Anycolor — who both hold together 70% of the market share in the Vtuber market, acting as an agencies or managers of these Vtubers and both are listed in Japan.

The first Vtuber that achieved popularity was Kizuna. Her success sparked a Vtuber trend in Japan, and it spurred the establishment of specialized agencies to promote them, including major ones such as Hololive Production (Cover Corp’s Agency) and Nijisanji (AnyColor’s Agency). Both players showed extreme growth during the last few years and both of them are very interesting to analyze. As VTubers gained mainstream popularity, brands and public institutions increasingly adopted them as marketing assets. Corporations such as SoftBank, Nissin Foods, Netflix, Sega, Taco Bell, and Honda have used VTubers or created original avatars to promote products and engage younger, digitally native audiences. This commercialization trend extended into merchandise and licensing further boosting the segment revenues of these companies.

My main issue of not buying shares is that the Vtubers are essentially a suppliers to agency like Cover Corp or Anycolor as they are fully managed characters. They make a living, but lots of them burns out very quickly. And more recently we have more and more examples of them going “independent” or in the industry terms “graduating”. This is a real risk to both of these agencies, because Vtubers are your best asset and once they leave/graduate, finding replacement or future top popular Vtuber is not easy. Another risk is that the growth has been slightly cooling off.

Tickets, tickets, tickets…

Then there is the largest ticketing platform in Japan called PIA corporation, which is essentially a Japanese ticketmaster. Interestingly, PIA is at the similar price to what it was during covid, despite obvious turnaround in its financials. Its business model allows this company what I would call “bonkers” free cash flow generation as people buy tickets from this distributor upfront but only after the event has performed actually PIA pays the event planners. In other words, PIA is being financed by suppliers. PIA operates in the oligopolistic market where three players have combined 90% market share, while it is estimated that PIA has roughly 50%. To give you of the an idea of the scale, they sold last year 85 million of tickets.

What caught my eye about PIA is that they made first ever price hike for a transaction fee or in other words for a fee generated per ticket sold by 50%. This has greatly helped to the bottom line. What I am not happy about with this company is valuation despite the extremely high OCF/EBIT conversion. The thesis would fall apart on assumption that after covid there was a pull-forward of the demand as people desired to travel and experience more events. PIA can leverage its massive scale and relationships by offering competitive take-rates to promoters. What further stands out is that PIA was an exclusive distributor for tickets to olympics.

Having the largest market share means that you would likely grow with the market from here. So what is the outlook for live events in Japan? The number of live events in Japan should grow by 6% a year and the company trades at 17x P/E at the moment. I struggle to see—except the huge cash conversion— the explosive growth that would make this investment asymetric.

Another reason I passed on this is that they do not have any succession in place as the CEO is approaching 77 years. That said, if we account for the cash and look at their FCF, it is clear that the company— being in the probably best live event market out there— looks truly interesting. The last reason I passed on it is poor capital allocation and cas hoarding.

I believe Japanese market today offers significant opportunities as investors focus solely on bottlenecks around AI theme. I am not that smart to judge the competition there I need to admit. But I think Japanese f(u)natism about entertainment is something as unique because and it is actually predictable—talk to your Japanese friend about it.

Japanese market also focuses on the short-term financials the most I have seen during my A-Z adventures. And lastly, they do not care about EV/FCF multiples. They care solely about P/E ratio and they punished lots of sectors because “AI is taking everything over”. I came to own conclusions regarding software and the impact of the AI that will be. However I believe this narrative made lots of one-foot hurdles and great opportunities even in companies that do not have remotely anything related to software.

Today’s agenda

Nevertheless, I have put together a write-up of the company I actually invested in and after answering the question: “Do I want to become a partner with this business” I decided to invest.

And for the second time, I borrowed this idea from my friend and investor who I look up to — David. David is a terrific investor and I recommend to everybody to follow him. What I am grateful about the most is that even though he maybe is not aware of that, he activelly makes me better investor and has significant influence over me.

It never hurts to put more eyeballs on the companies since there is only probably his and Made in Japan analysis out there as well as one write-up on Value Investors Club. I also like the fact that the company is something I look for now — simple tangible product or simple service, competittively advantaged at resonable valuation. It has numerous segments growing very fast, they are three times larger than the second largest competitor and Japanese investors punished it because of AI narrative. Despite growing sales 10x during the last 8 years, the company trades at 16x P/E and there remains significant opportunity for margin expansion as one of their segment that grows over 20% a year, has 75% EBIT margins.

With that, I am diving deep into what I believe unique, yet very misunderstood opportunity. So after buying into what I believe is unique industrial company last month, I have acquired 8.5% position in the company highlighted below, which I believe is truly great idea for the next three years. There are catalysts too in prices revisions and biggest buy-back authorization in the history. I will add commentary from persons who are actually close to the company by using their services.

This one stood out to me as unique after going through 1500 companies there already and if I could own only one Japanese company for the next 3-5 years I would own this one. I would describe this company with a takeaway from a book called hidden champions.

“Hidden Champions are companies that are little known to the public but are leaders in highly specialized niche markets. The future belongs not necessarily to the biggest companies, but to those that are best in a narrowly defined market.”

Or as Geoff Gannon would put it:

“Also, keep in mind that the best business is one that receives cash early on relative to when it records sales and needs little or no additional capital (plant, inventory, receivables, etc.) to grow the business. The less cash investment needed and the quicker the cash return on additional investment hits the coffers – the better the business is.”